USDT, US Banks & More Coincidences

Perhaps the greatest mystery in the financial markets today is “what is going on with Tether?” Well, here we lay out a little corner of the global banking system where a quantity of real USD seems to match Tether outstanding shockingly well. There is no question these are real USD. And there are circumstantial connections — strong ones — to parties close to Tether.

This is not saying “USDT is backed.” And it certainly is not saying “the folks behind Tether have always been honest.” But it is perhaps a first clue to what is really going on rather than simply clear evidence misrepresentation of some sort occurred.

So here is the plan. First we are going to go through two US banks that hold a lot of crypto-related USD. Then we are going to look how remarkably their balance sheets resemble the quantity of USDT outstanding. And finally we are going to hint at a fascinating connection between those banks’ purported source of USD and a potential “crypto big hitter” source.

US Banks

USD have their ancestral home in US banks. In this incredible interview the deputy CEO of Deltec Bank very incorrectly explains that USD can only sit in the US with US banks. Watch that interview not for accurate information — it contains a lot of true statements blended in with many many seriously false or confused ones. Rather watch it to get a sense for the misunderstandings which permeate the crypto markets. USD live all over the world. But the best place to hold USD from a liquidity or safety perspective is a regulated FDIC-insured US bank. We’re not talking return here, we are just talking safety and liquidity.

Two key US banks in the crypto economy are Silvergate and Signature. Just go to the Fireblocks integrations page and click the “fiat” button and these two pop up.

These are US banks. Lots of filings are available. As seems to have been the case last time we are going to read what nobody else has read.

Signature Bank

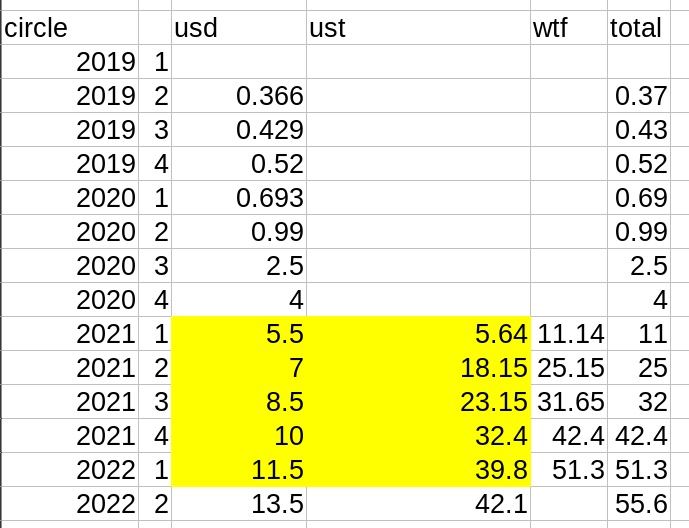

This bank has seen massive increases in deposits in the last few years:

Something happened in 2019 or 2020. And in fact Signature tells us some of what happened in their own words:

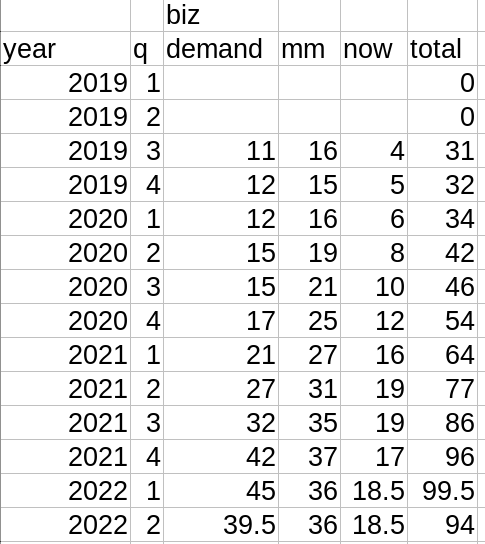

So it only remains to dig into the numbers. Signature bank does a wonderful job of breaking out the deposit base. For example:

So we can go ahead and aggregate a few years’ worth of these reports into a nice spreadsheet as follows. It’s only the business deposits we care about here:

Signature depends a lot on demand deposits. To a far higher degree than most large banks in the US. Signature notes this themselves:

Ok so Signature has a lot of business demand deposits, so what. Well they make clear these are from digital asset customers:

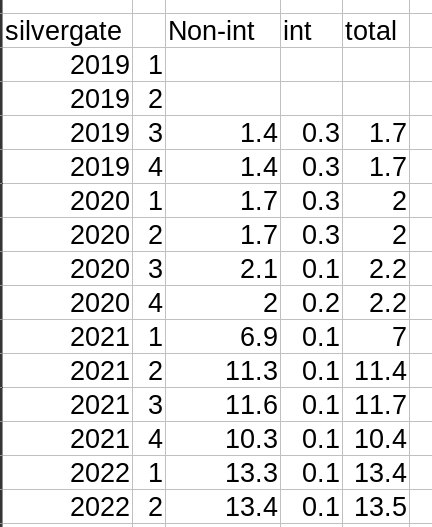

Silvergate Bank

Silvergate is also active in the crypto space:

And they have no real retail business. There is only one branch:

Ok so who are the customers? All kinds of folks from the crypto ecosystem:

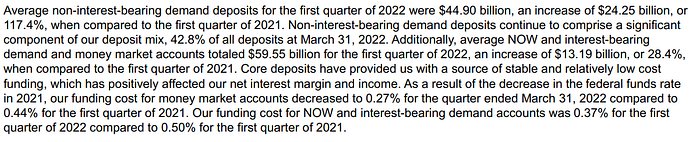

Fine. It should not be a hard sell that Silvergate also banks crypto businesses. And of course they disclose their deposit base:

They never have meaningful interest bearing accounts. It’s all non-interest bearing demand accounts presumably used for clearing. Again let’s just read all the reports and build a spreadsheet:

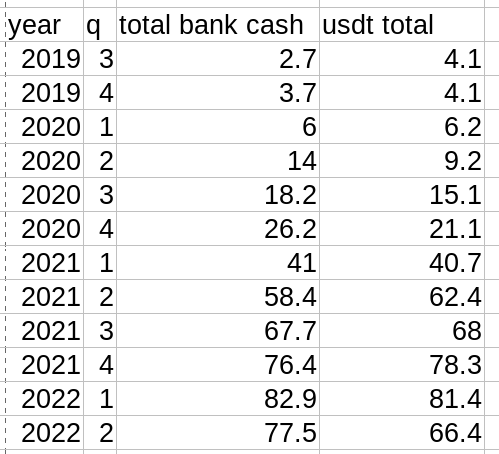

Putting Them Together

It’s pretty clear Silvergate was a tiny bank before this all started. But Signature was a real bank. So let’s add up their deposit bases but subtract off the 30 billion dollars Signature started with:

Some readers may recognize these totals. For they are shockingly similar to a famous total in the crypto space:

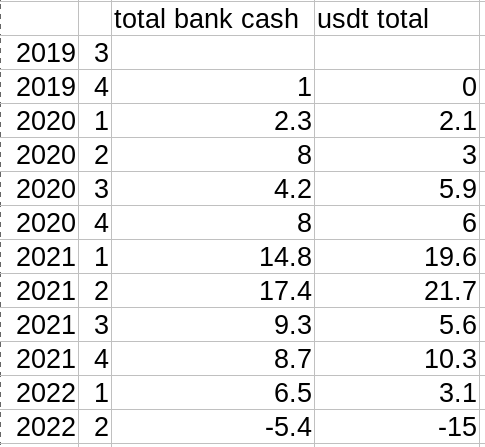

That’s right: it matches shockingly well the amount of Tether outstanding. This is perhaps even more striking when we look at the quarter-on-quarter changes:

There is absolutely no reason these numbers should have anything to do with each other naturally. Tether is not holding their cash reserves at these banks. Almost certainly; the banks should feel free to reach out otherwise.

Tether doesn’t even claim to have this much cash anymore. The reserve attestations include huge quantities of Treasury Bills for a while now.

And that last row? First the bank deposit amount is inferred from a different report so might be off. And the idea there was some sloppy deleveraging in crypto during 2Q 2022? Yeah that definitely happened. Give us credit for not just dropping the row entirely.

Also just to note: these USDT totals are taken from on-chain sources as the Tether disclosures do not cover the time period well:

Is It USDC?

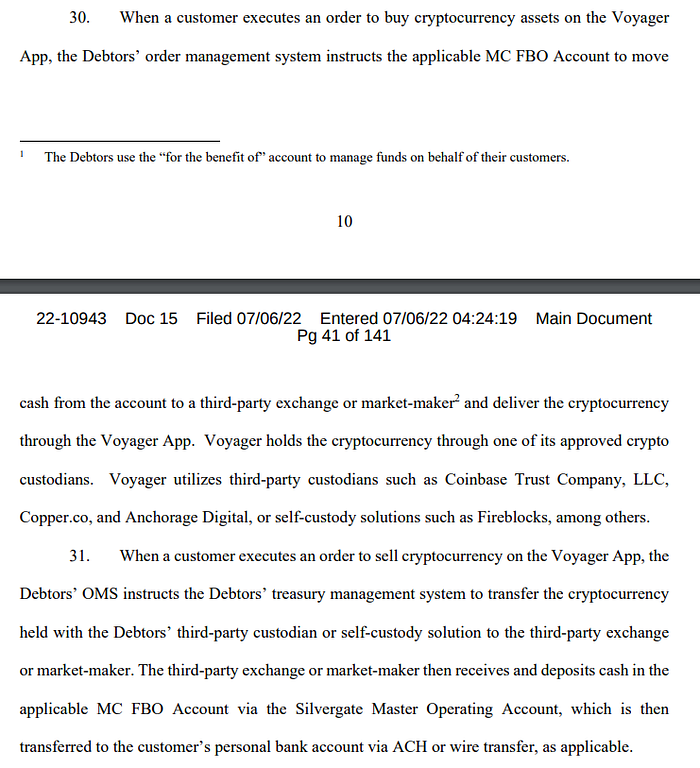

No. Why?

The end-2020 USDC attestation included only 4 billion of cash. Then USDC started giving wonky not-so-clear attestations for a while. And finally for 2Q 2022 they disclosed 13.5 billion of cash and 42.1 billion of Treasurys. While it is theoretically possible USDC was holding > 50 billion of cash at some point this table feels a lot more likely:

There is a meaningful amount of cash here vis a vis the 3AC yacht’s cost. But it is not really meaningful quarter-on-quarter when measured against USDT. The amazing correspondence between bank cash and USDT through 2020 and 2021 does not really depend on whether or not we include USDC. But the final total does. It seems safe to conclude these banks are not holding a material amount of USDC’s cash. Plus Circle clearly says the cash it at a range of banks including but not limited to these two.

There are error bars here and a few billion of USDC reserves in one of these banks won’t really change the analysis.

Other Banks

There are other banks associated with crypto in the US. But none of them is particularly large. Evolve is associated with a few debit card problems — but it’s entire balance sheet is under 1 billion USD. MVB also banks some crypto businesses. Its’ balance sheet hasn’t grown much at all and is about 2 billion the entire time.

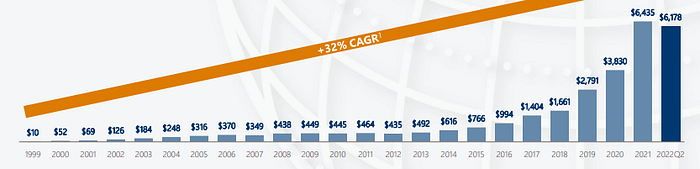

Metropolitan, of Voyager fame, has single-digit billion deposits. That might be relevant here at the margin as Metropolitan gained about 3 billion in deposits from 2019 to the present. Oh, and this slide from their IR presentation…you don’t need to be a data scientist to figure out the same stuff is going on as at Signature only in smaller size:

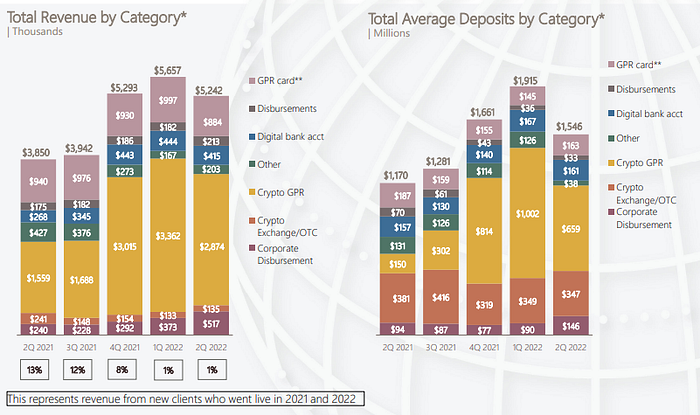

Oh, and look at this chart which explicitly shows information for “new clients who went live in 2021 and 2022” and even labels most of the money as crypto:

Now remember that Silvergate and Signature probably picked up some non-crypto deposits during this time too. 3 billion is 10% of the combined Signature+Silvergate starting balance sheet and 2% of the current one. Let’s just assume this all nets out and ignore the other banks. Next year that might not be safe but for now it probably is.

What Is Going On?

This is not Tether’s cash surely. At least not directly. But what is it?

First, this proves enough cash looks to have entered the ecosystem to back Tether. Absolutely nobody is claiming these US banks are lying about their deposit liabilities to both the SEC and FDIC. We have laughed at many a Bitfinex’ed tweet with the phrase “institutionalized investors”:

But yeah, someone sent money to these places. We are not asserting Tether has all of this cash or that they are honest. But it does look like enough cash came in one way or another. There is cash somewhere. We aren’t really saying they are dishonest either. The right amount of money is here.

Second, it suggests a theory. Maybe Tether’s commercial paper consists of obligations of whoever owns these USD deposits. Again there is money here and if one company promises it to another there is a sense in which that is commercial paper. It is a horrible abuse of the language but promising someone else your bank deposit is similarly some kind of a certificate of deposit or maybe cash-equivalent/accounts receivable thing.

This may not be right. But it is possible. We have written before about how the claims regarding Deltec and the Bahamian banking system were flawed. Nothing really fit or matched. No strong conclusions were available. We are now firmly convinced many of the points from this famous blog post were wrong but not for the reasons anyone expected.

This fits well. We have a theory which needs to wait for the next installment. But suffice it to say someone in the crypto ecosystem holds these dollars. A lot of people actually:

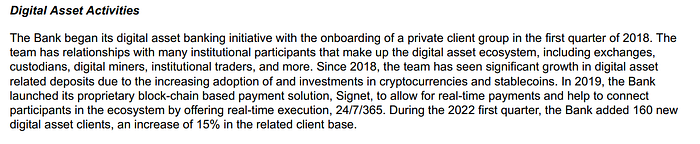

If 160 clients is a 15% increase in the digital asset client base they’ve got well over a thousand clients. That’s a lot! And a lot of retail funds flow through these mechanisms. Read this bit from the Voyager bankruptcy filings which makes plain retail dollars flow through the spreadsheets constructed above:

But enough about exchange USD deposits ending up here and Tether’s commercial paper possibly being circuitously backed by this cash. This post is already too long.

And Finally

This is not an attack or defense of Tether or Tether’s many critics. These truly may all be coincidences and accidents. That feels unlikely but it is of course possible.

Every single piece of information cited here comes from public sources — and generally public sources where there is a substantial penalty if one is caught lying. We don’t necessarily think anyone is lying. Over a year ago we wrote a blog post entitled “Tether: Maybe Everyone Is (Partially) Telling The Truth” which outlines a related theory and mechanism.

Finally things are starting to make sense overall. More coming soon…